What to Know Before You Buy a Medigap Policy

As I’ve mentioned, Medicare and Medical expenses can be one of your largest expenses in retirement, so it is critical that you choose the correct plan when you turn 65. This is my fifth in a series on Medicare. In this article I’ll share with you how to pick the best Medigap plan if you choose Original Medicare and a Medigap (Medicare Supplement) plus a drug plan.

As a reminder, you have two major choices for Medicare when you turn 65:

A. Original Medicare- from the federal government

Plus Medicare Supplement (Medicare Gap Plan) sold by for profit insurance companies

Plus Drug Plan sold by insurance companies (different for profit company)

B. Medicare Advantage from a for profit insurance company

Includes drug plan

Medigap plans are only for original Medicare enrollees.

They are sold by private insurance companies but regulated by states and the federal government. Original Medicare pays 80 percent of covered Part B health care services. Medigap insurance typically covers the 20 percent that is your responsibility to pay, along with some other health care costs. In contrast, a Medicare Advantage plan doesn’t allow supplemental insurance, even though it does have various out-of-pocket costs.

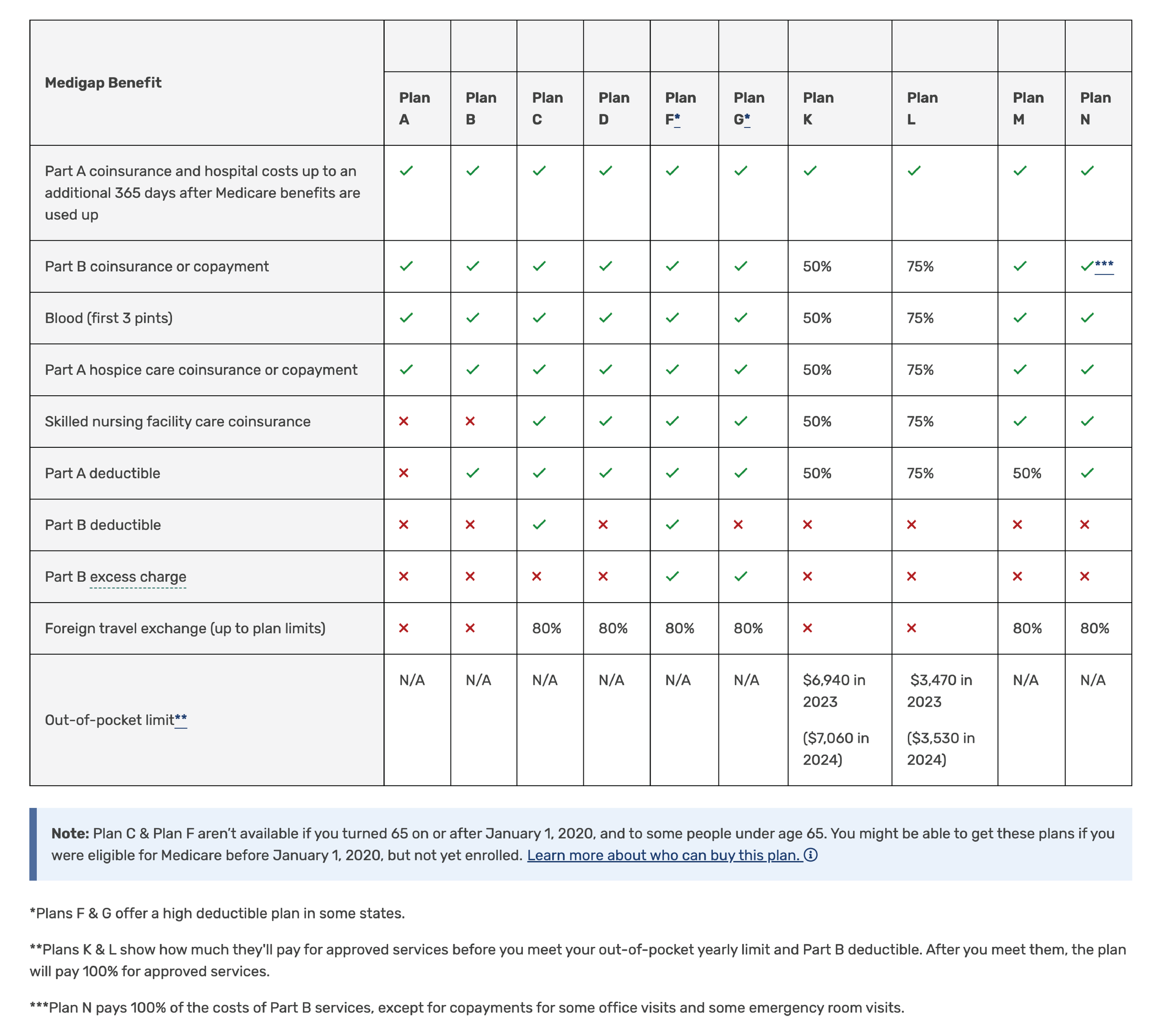

You likely have eight to 10 Medigap options.

The federal government, not insurers, determines what coverage a Medigap policy provides (except in three states: MA, MI, and WI). This is big. The Medigap plans cannot deny you coverage if the cost is approved by Medicare!!!! There are ten federally approved plans, each known by a letter: A, B, C, D, F, G, K, L, M and N. They’re standardized, meaning plans with the same letter name must provide the same basic benefits regardless of the insurer or location. It is more important which letter plan you select than which company provides it.

Policies are sold by private insurance companies.

This means you’ll likely have several choices of plans that have the same letter but are offered by different insurers in your locale. What they charge can vary dramatically.

The best time to buy a Medigap plan is when you first enroll in Medicare.

You can buy any Medigap plan available in your state — and insurers can’t turn you down or charge you more due to preexisting health conditions — during the six months after you initially sign up for Medicare Part B. After that, you could be denied or charged higher monthly premiums. It is also critical that you choose the plan that you will have for life. If you decide to switch Medigap plans in the future, you could be turned down due to your health.

“If you’re financially able to afford a Medigap plan, I would recommend you absolutely find the policy that’s best for you that provides the coverage you need, or may need down the road,” said Kristina Raner, program manager for the Medicare Improvements for Patients and Providers Act at the National Council on Aging. “We like to describe Medigap as like a marriage, says Raner. “You are choosing a plan and committing to it essentially forever, or as long as you’re able to pay the premium.”

Different plans have very different prices.

For example, a 65-year-old nonsmoking man in Fort Myers, Florida, could pay $64 a month for a Plan K policy or $263 for Plan D. A 65-year-old nonsmoking woman in Wichita, KS, might pay $32 a month for a high-deductible Plan G policy versus $455 for a regular Plan G.

Compare the benefits offered by each plan:

What Medicare Plan am I going to choose when I’m 65?

I know that the plan that I choose during the initial enrollment period at 65 is the plan that I will have for the rest of my life. My priority is to choose a plan that will allow me to choose the best facilities and doctors if I’m really sick. I’m willing to forgo the Medicare advantage extras such as Dental (few dentists take it), Vision, and gym memberships. I’m also willing to pay a higher premium to ensure that I have the best medical and drug coverage.

First I will schedule an appointment with Medicare Consultant Gene Ranney (941-716-4348) to do an analysis of which is the best Medigap plan for me. Gene Ranney helped my brother and sister-in-law pick the best Medigap and drug plan for them. I will pick the best Medigap category (currently G) and choose the company that he recommends. He will also do an analysis of the best drug plan for me based on my medications and where I like to buy it from. I know that unlike the Medigap Plan, I can switch drug plans every year.

NOT FINANCIAL ADVICE

The information contained in this article is for informational purposes only and shall not be understood or construed as financial advice. I am not an attorney, accountant or financial advisor, nor am I holding myself out to be. I do not accept any fees or commissions from anyone or any financial institution.

I’d love any feedback on these articles.