Long Term Care Insurance Dirty Little Secrets

In the last year of my mother’s life she was paying $120,000 a year for assisted living. Many of you with elderly parents have been shocked by the high cost of long-term care in assisted living facilities and nursing homes, or when employing home health aides. I’ve received numerous questions from readers about purchasing long-term care insurance (LTCI) to cover these costs. LTCI may seem like a great solution for covering the high cost of care in our twilight years, but is it really?

What is Long-Term Care insurance (LTCI)?

LTCI is designed to cover the costs of long-term care services, which typically include assistance with activities of daily living (ADLs) such as bathing, dressing, and eating. It can help with the costs of nursing home care, assisted living care, and home health care, which are not covered by Medicare. Although LTCI claims to provide a safety net as people age, it often leaves many policyholders in disastrous financial situations.

The LTCI offered today is not the same as your parents' LTCI.

For decades, the industry severely underestimated how many policyholders would use their coverage, how long they would live, and how much their care would cost. As the miscalculations sent profits plummeting, insurers raised premiums, reduced benefits, denied claims, and exited the market. Those insurers that remain in the market are often financially unstable, raising concerns about their ability to pay future claims.

No one tells you about rising premiums.

One of the most concerning issues with LTCI is that insurers may unexpectedly and rapidly increase premiums. Many policyholders purchase LTCI with the expectation of stable costs, only to face steep premium hikes as they grow older.

A policy holder quoted in The New York Times article “Why Long-Term Care Insurance Falls Short for So Many” has described LTCI as “a giant bait and switch.” Laura Lunceford, 69, of Sandy, UT, saw her annual premium for her policy with her husband leap from $3,800 to more than $5,700 in 2019. “[The insurer] had a business model that just wasn’t sustainable from the get-go,” she says. She feels sick to her stomach, she says, as the due date for her annual premium approaches, in fear that the insurer will demand another increase.

Premium increases like this can lead to policy lapses, as policyholders can no longer afford the coverage they have paid into for years. They lose all the money they’ve paid the insurance company and no longer have coverage.

Insurance companies make money by denying coverage.

Policyholders frequently encounter difficulties when trying to claim their benefits. The language in LTCI policies can be complex and filled with technical jargon that is difficult for the average consumer to understand. Insurers have been known to exploit this complexity, denying claims based on strict and sometimes ambiguous interpretations of policy terms. Common reasons for denial include not meeting the specific criteria for ADLs or the insurer’s definition of what constitutes necessary care. This can leave policyholders in dire straits, unable to access the care they need despite having paid premiums for many years.

These kinds of problems are very common.

In response to the New York Times article, a daughter shared:

”My mother died recently and [had] a Genworth policy. They worked hard to deny activating her coverage and, though she had [had] a stroke and was wheelchair bound, they insisted that she could ‘do too much herself’ to need her coverage to apply. After fighting for months, they finally approved her claim. Every three months, they required a video assessment and tried to cancel her claim at one point. Even when the claim was reinstated, they paid one out of twenty monthly invoices without a fight. They would insist that they could not read the uploaded bills in their portal, the care facility had a new item on the invoices, etc. It was a full-time job fighting with them and paying our lawyers to also fight with them. My father died quickly so Genworth kept all $350,000 of his available coverage; they made more than $200,000 in unpaid claims for my mother.”

A physician caring for an elderly patient commented on his experience with LTCI:

“Most long term care insurance is a scam. I have a 95-year-old independently living patient, a retired college professor, who has paid their premiums for decades and [has been] under my care for over 30 years. She has severe arthritis in both shoulders, arthritis in neck, diabetes, recently declared legally blind, heart failure on multiple medications and tried to access benefits for the 1st time early this year. The insurance company has dragged its feet for months, after I documented all the patient’s limitations on multiple occasions. I assume they hope these people will just die and they can keep their huge profits by delaying payment of appropriate benefits they promised to pay.”

Insurers will require a long waiting period after coverage has been approved, but before it can begin. They also cap total coverage.

A son commented in The New York Times:

“My mother’s policy has a 90 day waiting period. After 90 days our claim was denied by Genworth. I appealed and was told that appeals were taking a minimum of 45 days to be resolved. During that period the need for care still exists but you are in limbo awaiting a decision. Genworth finally approved the appeal but had caps on certain coverage.“

Once coverage kicks in, it’s typically capped at a certain daily or monthly amount, up to a lifetime maximum or a certain number of years.

How else can you afford to pay for long-term care?

Save and invest specifically for long term care. Instead of paying monthly premiums, invest monthly in a Roth IRA or brokerage account in a low cost S&P 500 index fund, like Vanguard (VFIAX) or Fidelity (FXAIX).

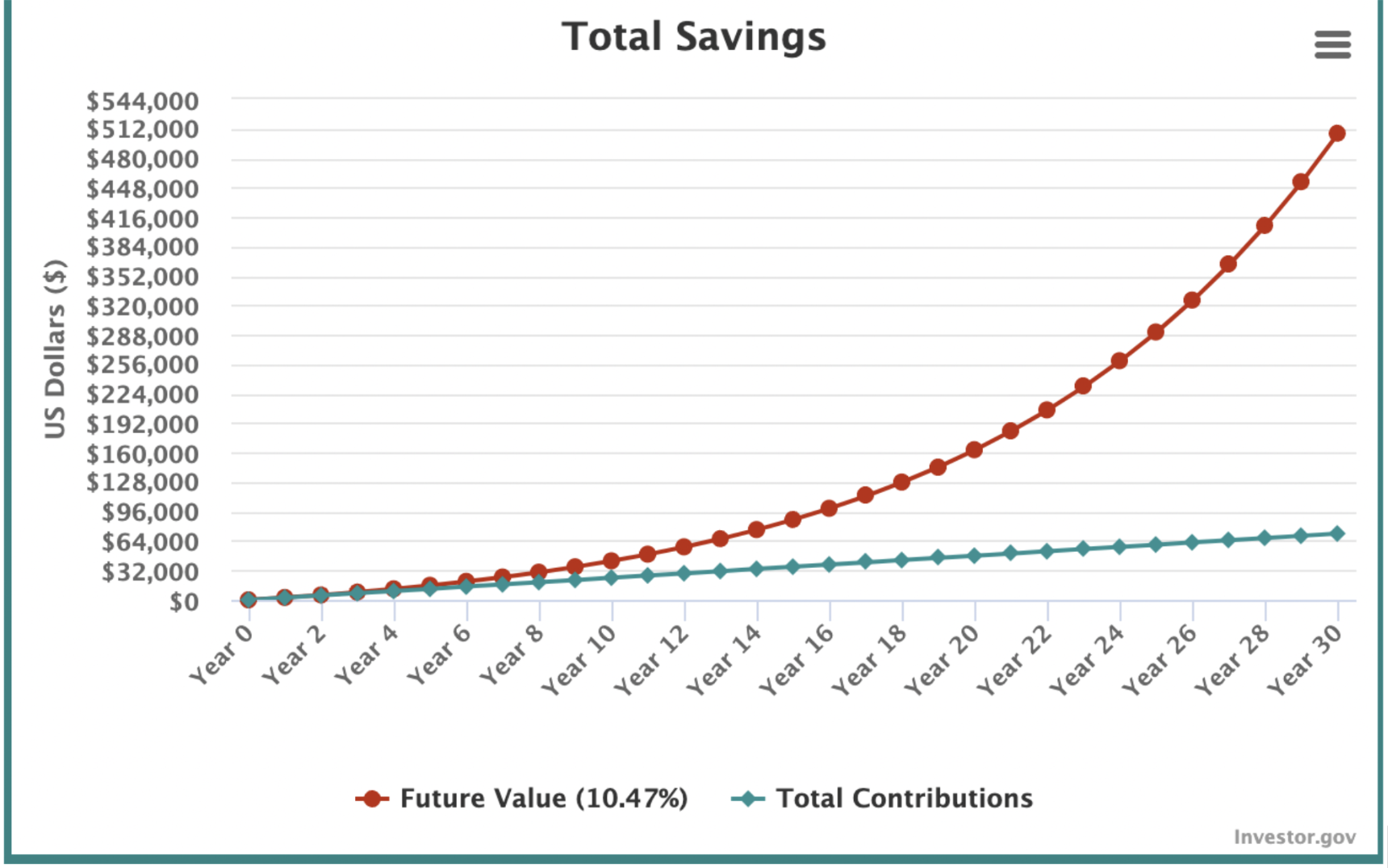

Let’s look at a case study.

A 55-year-old woman I’ll call Celeste is concerned about having enough money to pay for her long-term care as she ages. Celeste is eligible to invest in a Roth (IRA, 401k, or 403b) account while she is working and switch to a brokerage account after she retires. She decides to invest $200 per month in a low-cost S&P 500 Index fund for 30 years until she is 85.

According to Tradethatswing, the average yearly return of the S&P 500 over 30 years (ending April 2024) was 10.47%. Using this rate of return, Celeste’s investment of $72,000 will have grown to $506,970 by the time she turns 85, and she can use this money to cover the costs of her long-term care in any way she wishes. She will not have to pay taxes when she withdraws any of the money she deposits in a Roth (IRA, 401k or 403b). Any money deposited into a brokerage account she may have to pay Capital Gains Tax.

How will I handle the cost of long-term care?

I plan to pay for the costs of my long-term care with money that I have invested in my 401k. I don’t feel comfortable relying on an insurance company to cover these costs, especially considering we typically become more vulnerable as we age. While I was working, I saved money in my 401k that I earmarked specifically for long-term care.

Sources:

New York Times, “Why Long-Term Care Insurance Falls Short for So Many,” November 22, 2023

New York Times, “A Guide to Long-Term Care Insurance,” November 22, 2023

NOT FINANCIAL ADVICE

The information contained in this article is for informational purposes only and shall not be understood or construed as financial advice. I am not an attorney, accountant or financial advisor, nor am I holding myself out to be.